Marketing crack: Kicking the habit

o-CRACK-COCAINE-facebook

“We’ve created a gambling culture in which we tune out everything except the most immediate outcomes.”

Laurence Fink, Chairman and CEO, BlackRock

“Addiction is a pathological attachment to something attractive in the short term, but destructive over time. Recovery is about looking where we’re going and choosing a path that can last.”

Dr. Chris Johnstone, addiction specialist

IMPATIENT TIMES

Would you rather receive $100 today or $125 a year from now? Although a 25% increase is an excellent one-year return on investment, the average decision-maker would choose the smaller immediate gain rather than the larger future gain.

This tendency to discount the value of future gains is what psychologists call “temporal discounting” and what economists term “rates of time preference.” It’s what you and I would call patience. And we live in impatient times.

The short-termism of the corporation has been well-documented:

While typically, between 70 and 90 percent of a company’s value is related to cash flow expected three or more years out, management tends to be preoccupied with what’s reported three months from now. And as Dominic Barton of McKinsey observes, "If the vast majority of most firms’ value depends on results more than three years from now, but management is preoccupied with what’s reportable three months from now, then capitalism has a problem."

In the UK and US, cash-flows 5 years ahead are discounted at rates more appropriate 8 or more years hence; 10 year ahead cash-flows are valued as if 16 or more years ahead; and cash-flows more than 30 years ahead are scarcely valued at all.

In 1995, the mean duration of departing CEOs from the world’s largest 2,500 companies was just under 10 yrs. By 2009, it had fallen to around 6 years.

In the 1960s, 40% of US corporate earnings and borrowing used to go into investment. By the 1980s, that had fallen to 10%.

S&P companies spend 95% of their profits on share buy backs and dividends - $914 billion - rather than on long-term investment

Between 2004 and 2013, $3.4 trillion was spent on share buy backs at the expense of long-term investment

The long is, as Andrew Haldane, Chief Economist and the Executive Director of Monetary Analysis and Statistics at the Bank of England has put it, is short.

We can hold the gospel of shareholder value responsible for much of the short-termism that plagues so much of capitalism. First espoused by Milton Friedman in 1970 it holds that the singular goal of a company should be to maximize the return to shareholders. But in placing shareholder value before everything else, it encourages corporations and their management to focus on increasing the stock price, while doing little to encourage long-term investment.

To this, we’ve added the fuel of turbocharged data.

Information - and with it our capacity to acquire, disseminate, and respond to it - continues to accelerate at dizzying rate. Moore’s Law continues to make its rampage through our times, rewiring lives, markets, business, and expectations. It compresses everything it touches - distance, time, the feedback loop of the marketplace, our boredom threshold, our capacity for patience.

Consider that while news of Nelson’s victory in 1805 at the Battle of Trafalgar took 17 days to reach London (2.7mph), news of the Sichuan earthquake in 2008 took just 1 minute reach London (204,000mph).

Or that the average tenure of Premiership football managers has fallen by one month per year since 1994. If this trend continues, it will fall below one season by 2020.

Or that we’ve come to expect things so quickly that we can’t wait more than a few seconds for a video to load. Analysis of the viewing habits of 6.7 million internet users has revealed that after 2 seconds people start abandoning. After five seconds, the abandonment rate is 25 percent. When you get to 10 seconds, half are gone.

As the novelist and cultural observer Douglas Rushkoff has recently argued, immediacy is more and more the central defining characteristic of our culture:

Our society has reorientated itself to the present moment. Everything is live, real time, and always-on. It’s not a mere speeding up… It’s more of a diminishment of anything that isn’t happening right now. So much so that we are beginning to dismiss anything that is not happening right now – and the onslaught of everything that supposedly is.”

The forces that are transforming culture and capitalism run through our business too. For as capital and management have become increasingly impatient, we have inevitably (and in large part unwittingly) become both slave to and enabler of their agenda and rate of “time preference”.

We too have reorientated ourselves to the present moment.

CHASING SHORT-TERM METRICS

Digital interactions have brought us a wealth of new data.The lure of this data is not only that is it immediately available, but that much of is highly responsive to marketing activity.

Under pressure to account for our activities and to show that they are having an effect (any effect) and hooked on the crack cocaine of the short-term, we seize on intermediate metrics such as likes, views, tweets, shares and so on, like crazed junkies desperate for the next fix.

This data might be exciting, it might be highly responsive to communications activity, it might be easy to measure, and it might give us impressive sounding numbers to use in case study videos, but it is short-term data that tells us nothing about the long-term business effects of our efforts.

Worse, our holding up of short-term metrics that simply measure the exposure of consumers to our ideas as evidence of our success relegates our contribution to the mere distribution of content. And so - such is our appetite for evidence that something happened in the short-term - we relentlessly conspire to render the creation of enduring ideas, the building of memories, the shaping of perceptions, preferences, and behaviours a trivial side-show. The very things which that are the source of our value as an industry, and the generators of sustainable value for brands and businesses.

The short-term is invariably easier to manage and measure than the long-term. Yet as Binet and Field cautioned in their first round of analysis based upon the IPA’s DataBank what is important, and what is easy to measure, are not always the same thing. We forget the distinction between the important and the easy at our peril.

INCREASINGLY FIXATED WITH DEMAND FULFILMENT

Such is the gravitational pull of the short-term that we can stand idly by, mute, uncomprehending, or complicit, when we’re told that the future lies in ever tighter targeting and the pursuit of ever greater relevance.

Central to the promise of programmatic media buying is greater efficiency through improved relevance - getting the right content in front of the right person. But it carries risks in equal measure to its rewards. The co-author of the celebrated Cluetrain Mainfesto Doc Searls unwittingly articulates the dangers of blindly pursuing efficiency and hyper-relevance perfectly: “The Intention Economy grows around buyers, not sellers. It leverages the simple fact that buyers are the first source of money, and that they come ready-made.”

Of course the better targeted any marketing programme is, the higher the response rate. The gain in efficiency comes from not trying to sell things to people who aren't interested. Thus as one agency puts it: "with this type of automated advertising, you know your ad impressions will only be used on certain people who are already interested in your product or service.”

But once again we conflate effectiveness and efficiency. Response rates are proportional, as the marketing scientist Byron Sharp reminds us, and don't say anything about total effect size. A 50% response from targeting 100 peopleafter all, is less than a 10% response from mailing to 1000 people.

Tighter targeting delivers higher response rates, but the pursuit of efficiency cannot be allowed to drive out the pursuit of effectiveness.

Nor can the visibility of consumer interest and intent to the marketer allow us to shrink our horizons, and relocate our contribution down to the very last step in the path to purchase. The insistence that the task of modern marketing is demand fulfilment amongst the already interested is to give up on the very idea of brand-building.

FAILING TO CELEBRATE LONG-TERM BUILDERS

There is perhaps no better barometer of our industry than what we choose to reward. And here the evidence is telling. Aside from effectiveness awards, there is no forum which celebrates the brand-building work of sustained creativity and succeeds in attracting both clients and creative agencies.

The Cannes Effectiveness Lion is a notable and welcome exception to this. But it proves the rule that - as John Hegarty noted at last year’s Cannes Lions Festival - creative awards are inherently about creative innovation.

Small wonder that that creatives juries are biased against work that forms part of a long-running campaign. It’s just “not new’.

RECOVERING OUR PURPOSE

As Lawrence Green has put it, this is marketing mission drift, “from an art practised for the longer-term health of a brand and business, to a science lopsidedly focused on the short term.”

It is addiction - a pathological attachment to something attractive in the short term, but destructive over time.

Adland is in much need of a reformation, and our first step to recovery should be to remind ourselves that brand-building is by its very nature, a long term business.

That would might seem to be so self-evident as to be redundant, and yet some extraordinarily misguided, inaccurate (or plain self-serving) claims for how advertising works continue to be peddled.

This, for example, is how some (otherwise respectable) folk have represented advertising - as a being fundamentally activity that only has a short-term effect:

charts.001

Respectable or not, this is bullshit.

The fact of the matter is that most advertising simply does not pay back in the short term. And a succession of short-term effect activation or promotional effects will invariably fall far short of the gain that comes from pursuing long-term effects.

The effect is not just the driving up of volume or share, but pricing improvements. And as the analysis undertaken by Les Binet and Peter Field of thirty years’ of IPA Effectiveness Awards data demonstrates, the most profitable of all campaigns are those that drive both incremental volume and the strengthening of margins. And since pricing effects are slower to crystallise than volume effects this takes time.

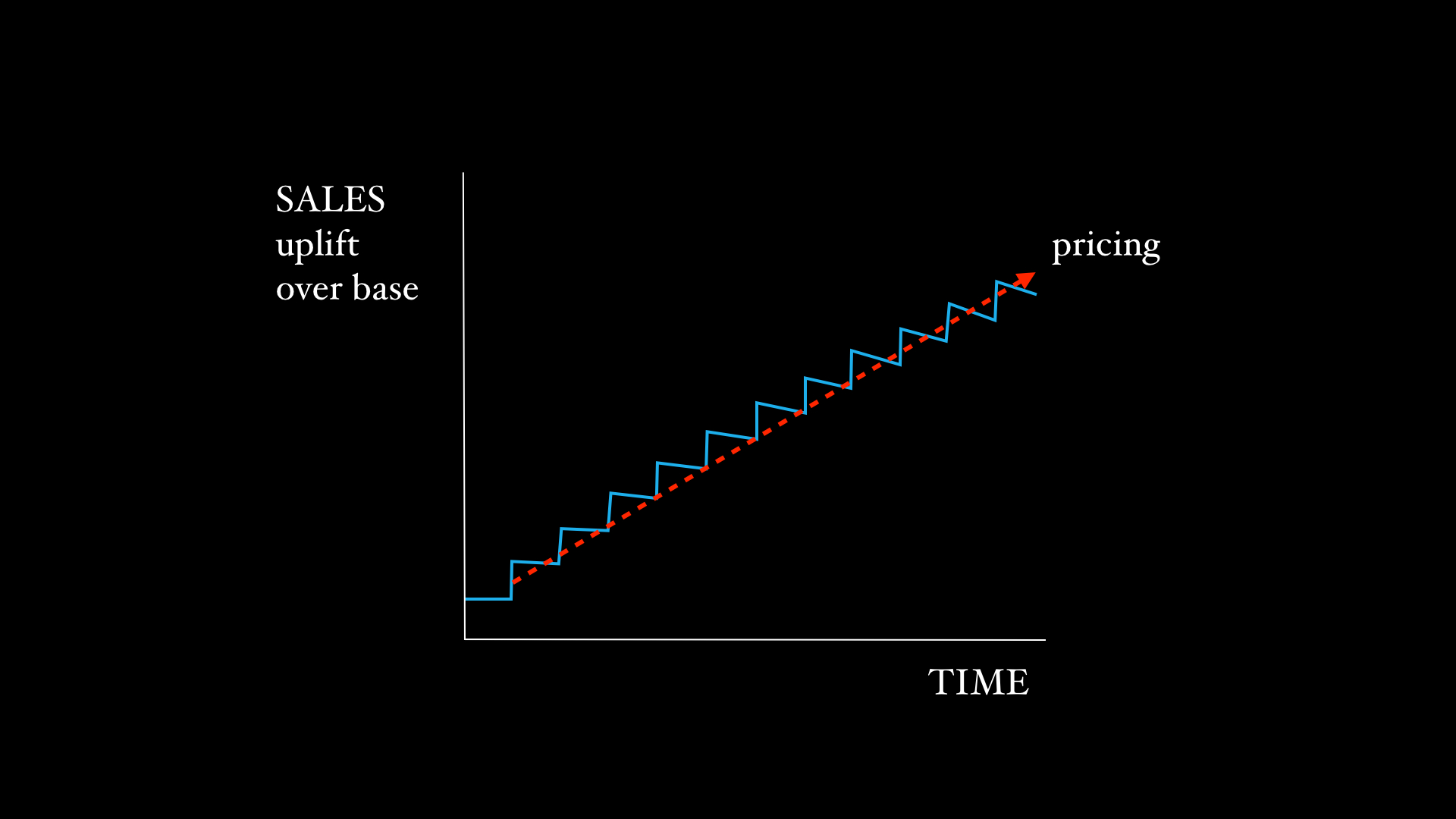

So this is what long-term brand-building actually looks like:

CHART > LONG TERM EFFECT.001

Over time, baselines sales (i.e the volume that is bought at full, not discounted price) are - along with pricing - nudged upwards.

And the means by which this is accomplished is through the intangible, the stirring of emotions, the creation and nurturing of what Bryon Sharp terms memory structures, what Judith Williamson called "empires of the mind", and most of us would call brand-building.

This is not to argue that the short-term does not matter at all. After all there can be no ‘tomorrow’ for a business if there is no ‘today’. As Jack Welch, the former CEO of GE has said, “the job of a leader and his or her team is to deliver to commitments in the short term while investing in the long-term health of the business”. Brands do need to direct some of their investment towards short-term activations that leverage the brand’s equity and produce short-term sales while the brand builds momentum.

But the short-term cannot be the focus or priority.

For it is the curve that ultimately matters, not the blip.

***

A PATH THAT CAN LAST

We are an industry in the grip of an existential crisis, looking over with confusion at the powerhouse players in adjacent industries, and envying their apparent confidence and their power to disrupt. So I hesitate to suggest that we might look to others to remind us what we are about, for a new metaphor to create by, and perhaps, and a better standard to hold ourselves account to.

But the platform builders do were to remind us of the value of thinking big and thinking long.

#1 TAKE THE LONG VIEW

Whether it is Google, Facebook, or iPhone, the business of platforms is inherently a long-term one.

Here for example, is Brin and Page’s first ever letter to shareholders in 2004:

As a private company, we have concentrated on the long term, and this has served us well. As a public company, we will do the same. In our opinion, outside pressures too often tempt companies to sacrifice long term opportunities to meet quarterly market expectations… If opportunities arise that might cause us to sacrifice short term results but are in the best long term interest of our shareholders, we will take those opportunities… We recognize that our duty is to advance our shareholders' interests, and we believe that artificially creating short term target numbers serves our shareholders poorly. We would prefer not to be asked to make such predictions, and if asked we will respectfully decline. A management team distracted by a series of short term targets is as pointless as a dieter stepping on a scale every half hour.”

And as Jeff Bezos remarked in an interview, taking the long view is a source ofcompetitive advantage:

If everything you do needs to work on a three-year time horizon, then you’re competing against a lot of people. But if you’re willing to invest on a seven-year time horizon, you’re now competing against a fraction of those people, because very few companies are willing to do that.”

The achievements of Sir Alex Ferguson, the manager of Manchester United from 1986 to 2013 show this in action.

The hallmark of his management of the club was that he took the long view. As he said in an interview for Harvard Business Review:

The first thought of 99% of newly appointed managers is to make sure they win—to survive. So they bring experienced players in. That’s simply because we’re in a results-driven industry. At some clubs, you need only to lose three games in a row, and you’re fired. In today’s football world, with a new breed of directors and owners, I am not sure any club would have the patience to wait for a manager to build a team over a four-year period. Winning a game is only a short-term gain—you can lose the next game. Building a club brings stability and consistency. You don’t ever want to take your eyes off the first team, but our youth development efforts ended up leading to our many successes in the 1990s and early 2000s. The young players really became the spirit of the club.”

His focus was always on building a successful club (the long view), not just a successful team (the short view).

Ferguson stood down as Manchester United boss at the end of his final season, having won 49 trophies in the most successful managerial career British football has ever known.

#2 EMBRACEBIG IDEAS

Joseph Jaffe has argued that:

Big ideas take too much time to find and we don't have the time to find 'em (not on current accountability time). Big ideas are equated to expensive ideas...hence the word BIG. They're meant to create a splash; secure buzz; enrapture the masses with pomp, grandeur and ceremony. Big ideas are similarly, full of hot air, fluff, inflated with self-importance, exaggeration and hyperbole.”

Oh yes, how much more prudent, agile, spendthrift, modest, humble, properly authentic, and just downright more au courant, to pursue a bunch of small ideas.

Except that you need a big, organising idea if you are to have something to navigate by over the long-term.

If you are to make the most efficient use of the finite resources available.

If you want activity to aggregate its effects.

If you are to have a rich source of inspiration for the long term.

If you are to recruit, galvanise, organise, and focus resources over the long-term.

If you are to have customers keep returning to you over the long-term (and recognize you when they look for you or come across you).

When big gets a bad name (and is often deliberately conflated with scale of production budget), we might want to recall the words of Peter Thiel:

Iteration without a bold plan won’t take you from 0 to 1.”

#3 MAKE AGILITY PURPOSEFUL

The wonderful thing about having a long-term direction is that it makes flexibility and responsiveness possible. As the military historian and management consultant Stephen Bungay puts it:

Strategy is essentially an intent rather than a plan, because the knowledge gap means we cannot plan an outcome but only express the will to achieve it, and the effects gap means that we cannot know for certain what the effects of our actions will be, and that we will probably have to modify our actions to achieve the outcome we want. We can only do that if we are clear about what outcome we desire.”

Laurence Freedman (also a military historian) too, makes the same point in his magnum opus Strategy: A History:

Strategy is much more than a plan. A plan supposes a sequence of events that allows one to move with confidence from one state of affairs to another… Strategy is required when others might frustrate one’s plans because they have different and possibly opposing interests and concerns… The inherent unpredictability of human affairs, due to the chance events as well as the efforts of opponents and the missteps of friends, provides strategy with its challenge and drama… Strategy is often expected to start with a description of a desired end state, but in practice there is rarely an orderly movement to goals set in advance. Instead, the process evolves through a series of states, each one not quite what was anticipated or hoped for, requiring a reappraisal and modification of the original strategy, including ultimate objectives.”

Because they can distinguish between plans and strategy, they’re able to focus on the long-term game, and be able to respond to events and circumstances at the same time.

Facebook’s self-declared mission (aka big idea) is “to give people the power to share and make the world more open and connected” gave it the flexibility to modify its actions, and start building value on what it had previously ignored. The one digital device set to dominate them all, namely mobile.

Much has being said and written about the need for corporations and marketers to increase the tempo of their efforts. That Facebook now makes 69% of its revenue from mobile illustrates the other advantage of long-term strategy. It makes speed purposeful. As Lawrence Green has sagely noted:

The faster you are going to execute, the more precise and commonly understood your direction of travel must be. Pace is only an asset, warned Arsene Wenger as he introduced Theo Walcott, if you know where to run. Hold the great Frenchman’s thoughts in mind as your answer the ever more urgent call to seize the day, to answer to now.”

#4 EXTRACT MAXIMUM VALUE FROM YOUR PLATFORM

Not everything of course is as malleable as software. If you’re running a business that is dependent on tangible assets and infrastructure, then ‘pivoting’ is probably going to be a far more challenging affair than if you’re running a business that’s built on lines of code.

However, what does characterise the successful platform builders is that they don’t change the platform every two years.

But they do build new things on it.

For example, booking.com’s boookingnow app represents another way of delivering the perfect accommodation solution - ‘the delight of right’ - to late or spontaneous bookers, making their arrangements on their phone. But the platform mission of delivery more delight of right moments to more travellers remains.

Rather than change the platform every three years, we’d be better off building new things on it.

#5 BUILD A PLATFORM OTHERS WANT TO BUILD UPON

Which brings me on to the next point. Many modern platforms are all about making themselves available for external application development.

The iPhone for example, would not be the generating the $47 billion it did in 2011 without the apps that have been created for it. From Facebook to Angry Birds, Uber to Candy Crush these have created immense value for Apple that they never would have realized on their own.

Opened last year, Nike’s Nike+ Fuellab is a collaborative work and testing space for selected partner companies to develop products that integrate the NikeFuel system for tracking and measuring activity.

Platforms provide the infrastructure others can create upon to build value.

And good brand platforms are little different.

The opportunity provided for example, by Old Spice’s Smell Like a Man platform has ensured that creatives clamour to work on the P&G business.

This isn’t an argument for selfish creative indulgence.

Brand platforms must be sustained over the long-term, so the importance of ensuring that creative minds (of all kinds) can sustain their creativity and enthusiasm over the long term cannot be underestimated.

#6 BUILD AROUND THE NEEDS OF PEOPLE

If the new adjacent industries, and their digital products, services and platforms do anything, it is to remind us to build around the needs of the user/customer/consumer. As Peter Thiel argues “The best entrepreneurs know this: every great business is built around a secret that’s hidden from the outside. A great company is a conspiracy to change the world”.And the best way to find secrets, is to look for the unsolved and unanswered problems in people’s lives.

It is time we all got back to properly building long term sustainable futures for our client businesses and brands - and time that businesses as Giles Hedger has put it, “seek to grow in step with human development not in an accelerated parallel universe.” This shift, Dominic Barton argues, is not just about managing for the long-term and how we manage and lead corporations. It’s also about changing what we believe is a business’s value and role in society.

Writing for Forbes, Steve Denning surveys the unforeseen consequences of the narrow and relentless pursuit of shareholder value:

Endemic short-termism

Combines of executives and shareholder

Executive cronyism

Widespread stock price manipulation

The undermining organisations, communities and whole industries

Dispirited employees

A failure to renew human capital

Short-changed customers

Obsolete management practices

Economic stagnation

International uncompetitiveness

Rampant income inequality

An unhealthy concentration of economic power

Successive economic crashes

An unhealthy concentration of economic power

And a corrupted society

The voices calling for a reformation of the corporation, a rethinking of its priorities, and an end to the the myopic pursuit of shareholder value above all else are impressive. And growing.

Vinci Group Chairman and CEO Xavier Huillard has called theidea of maximising shareholder value “totally idiotic.”

Alibaba CEO Jack Ma has said that “customers are number one; employees are number two and shareholders are number three.”

Paul Polman, CEO of Unilever has denounced “the cult of shareholder value.”

John Mackey at Whole Foods has condemned businesses that “view their purpose as profit maximization and treat all participants in the system as means to that end.”

Marc Benioff, Chairman and CEO of Salesforce has declared in an article in the Huffington Post that “the business of business isn’t just about creating profits for shareholders - it’s also about improving the state of the world and driving stakeholder value.”

And Tim Cook, CEO of Apple when asked to disclose the costs of Apple’s energy sustainability programs, and make a commitment to doing only those things that were profitable, replied, “When we work on making our devices accessible by the blind,” he said, “I don’t consider the bloody ROI.” It was the same thing for environmental issues, worker safety, and other areas that don’t have an immediate profit. The company does “a lot of things for reasons besides profit motive. We want to leave the world better than we found it.”

Roger Martin dean of the Rotman School of Management at the University of Toronto, contrasts the agenda of shareholder capitalism and its focus on investor expectations, with the agenda of consumer capitalism, in which real factories are built, real products produced, real revenues are earned, and real dollars of profit show up on the bottom line:

The difference in outcomes between a real-market focused world and an expectation-market dominated world is stark and critically important for the economy. When the real market is dominant, customers are the focus and the central task of companies is to find ever better ways of serving them… When the expectations market is dominant, traders are the focus and gaming markets is the task…. the expectations game is beginningto destroy the real game, slowly from within… Companies should place customers at the centre of the firm and focus on delighting them, while earning an acceptable return for shareholders.”

As those charged with understanding the real, day to day lives, needs and wants of ordinary people, we in the marketing community have a unique and privileged perspective that the majority of those in the C-suite - far, far removed from the lives, concerns, dreams, struggles, aspirations and joys of the 99% - are not privy to. And we should recognise that with this perspective comes a responsibility.

We should be lending our voice in calling for a wholesale reformation of the corporation, for a refocusing of our efforts on long-term value creation not short-term value extraction, and for building long-term sustainable futures around the needs of the customer.

***

“The untutored savage, like the child” wrote the nineteenth century economist William Jevons, “is wholly occupied with the pleasures and troubles of the moment; the morrow is dimly felt; the limit of his horizon is but a few days off.”

It's time for a shift in our priorities.

In our perspectives.

In what we value.

And in what we build.

It’s time we all grew up.

***

This is the long copy version of a presentation given at the 2015 FutureFlash conference. My thanks to the gang at Contagious for the opportunity to participate, and to Canada's Institute of Communications Agencies for being such welcoming hosts as well as a great audience.

***

SOURCES

Dominic Barton, ‘Capitalism for the long term’, Harvard Business Review, March 2011

Les Binet & Peter Field, Marketing in the era of accountability

Les Binet & Peter Field, The Long and the Short of it: Balancing Short and Long-Term Marketing Strategies

Bloomberg Business, ‘S&P 500 companies spend almost all profits on buybacks’, 6 October 2014

Sue Bridewater, ‘End of season football manager statistics for 2013-14’

Stephen Bungay, The Art of Action: How Leaders Close the Gaps Between Plans, Actions and Results

Avi Dan, ‘The Kardashian effect: The short-lived client-agency romance’, Forbes, February 29th 2012

Steve Denning, 'The unanticipated risks of maximizing shareholder value', Forbes, 14 October 2014

Anita Elberse, ‘Ferguson’s forumla’, Harvard Business Review, October 2013

The Economist, ‘The repurchase revolution’, 13 September 2014

Larry Fink, letter sent to Fortune 500 CEOs, 21st March, 2014

Lawrence Freedman, Strategy: A History

Milton Friedman, 'The social responsibility of a business is to increase its profits', The New York Times Magazine, September 13, 1970

Google, ‘Measure what happens most’

Andrew Haldane, The Short Long, 29th Société Universitaire Européene de Recherches Financières Colloquium: New Paradigms in Money and Finance?, Brussels, May 2011

Andrew Haldane, ‘Growing, fast and slow’, speech at University if East Anglia, 17 February 2015

Andrew Haldane, ‘Patience and finance’, speech at Oxford China Business Forum, Beijing, 9 September 2010

Giles Hedger, ‘Marketing in the age of sustainability’, Admap January 2010

Joseph Jaffe, ‘A small idea (death of THE big idea)’

The Kay review of UK equity markets and long-term decision making, final report, July 2012

S. Krishnan & R. Sitaraman, ‘Video Stream Quality Impacts Viewer Behavior: Inferring Causality Using Quasi-Experimental Designs’

Roger Martin, Fixing The Game: How Runaway Expectations Broke The Economy, And How To get Back To Reality

Roosevelt Institute, ‘The disconnect between corporate borrowing and investment’, 25 February, 2015

Douglas Rushkoff, Present Shock: When Everything Happens Now

strategy&, ‘CEO succession 2000-2009: A decade of convergence and compression’, 25 May 2010

Peter Thiel, Zero to One: Notes on Startups, or How to Build the Future

John Tomlinson, The Culture Of Speed: The Coming Of Immediacy

The Wall Street Journal, ‘CEO tenure, stock gains often go hand-in-hand’, 6 July 2010